Price action like that reflects a specific thesis: that the business is more vulnerable to the rate environment than its financials suggest. The Value Meter looks past that thesis and focuses directly on the numbers. What it finds is worth examining.

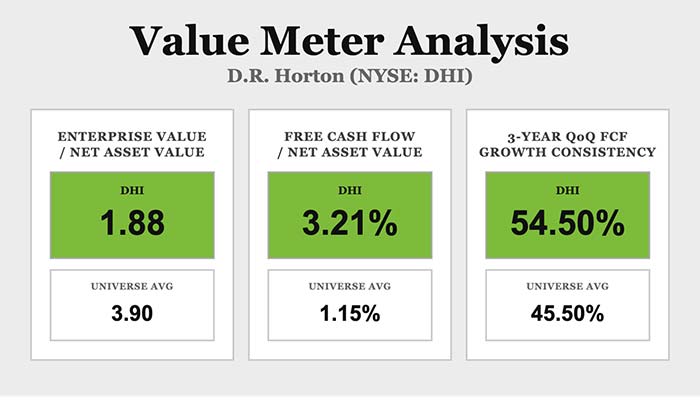

Price action like that reflects a specific thesis: that the business is more vulnerable to the rate environment than its financials suggest. The Value Meter looks past that thesis and focuses directly on the numbers. What it finds is worth examining.  D.R. Horton’s enterprise value is 1.88 times its net asset value, roughly 52% below the broad market average of 3.90. A discount of that size does not reflect indifference. It reflects a market assigning a risk premium that the company’s own balance sheet does not justify. Buyers at today’s price are effectively acquiring $1 of assets for around $0.48. The company’s quarterly free cash flow relative to net asset value is 3.21%, compared with a broad market average of 1.15% – nearly 180% above average. That gap has a practical consequence: A business generating cash at that rate while priced at a steep discount is compounding its margin of safety – the difference between the intrinsic value of the business and its lower market value – quarter by quarter. Furthermore, over the past three years, D.R. Horton’s quarterly free cash flow has grown sequentially about 55% of the time, against a broad market average of about 46%. That is not a streak of fortunate quarters. It is a result of the company’s business model sustaining positive cash flow momentum across rising rates and uneven demand. For an investor entering at a significant discount, that consistency matters. Even if conditions take a while to improve, the downside for the stock remains manageable. One quick note: A reader named Timothy recently asked me whether The Value Meter’s “universe averages” are based on industry competitors or the entire market. The answer is the latter. Most analysts, for good reason, tend to compare individual companies with firms that have similar business structures, incentives, tailwinds, headwinds, etc. By doing so, they can determine a company’s relative position against its peers. The Value Meter, however, offers a bird’s-eye view. It’s telling us something broader about the market and about the stocks it analyzes. Considering the cash flows the company generates, is its acquisition cost really that worthwhile? D.R. Horton: Is “America’s Builder” a Bargain Right Now? appeared first on Wealthy Retirement.

D.R. Horton’s enterprise value is 1.88 times its net asset value, roughly 52% below the broad market average of 3.90. A discount of that size does not reflect indifference. It reflects a market assigning a risk premium that the company’s own balance sheet does not justify. Buyers at today’s price are effectively acquiring $1 of assets for around $0.48. The company’s quarterly free cash flow relative to net asset value is 3.21%, compared with a broad market average of 1.15% – nearly 180% above average. That gap has a practical consequence: A business generating cash at that rate while priced at a steep discount is compounding its margin of safety – the difference between the intrinsic value of the business and its lower market value – quarter by quarter. Furthermore, over the past three years, D.R. Horton’s quarterly free cash flow has grown sequentially about 55% of the time, against a broad market average of about 46%. That is not a streak of fortunate quarters. It is a result of the company’s business model sustaining positive cash flow momentum across rising rates and uneven demand. For an investor entering at a significant discount, that consistency matters. Even if conditions take a while to improve, the downside for the stock remains manageable. One quick note: A reader named Timothy recently asked me whether The Value Meter’s “universe averages” are based on industry competitors or the entire market. The answer is the latter. Most analysts, for good reason, tend to compare individual companies with firms that have similar business structures, incentives, tailwinds, headwinds, etc. By doing so, they can determine a company’s relative position against its peers. The Value Meter, however, offers a bird’s-eye view. It’s telling us something broader about the market and about the stocks it analyzes. Considering the cash flows the company generates, is its acquisition cost really that worthwhile? D.R. Horton: Is “America’s Builder” a Bargain Right Now? appeared first on Wealthy Retirement. Source: https://wealthyretirement.com/income-op ... source=app