Energy markets have been anything but calm, with shifting oil prices and investor skepticism keeping midstream stocks under pressure. Yet beneath that volatility, some companies continue to generate steady cash and return capital – even as their valuations lag the broader market.

Plains All American Pipeline (Nasdaq: PAA) is a major crude oil midstream operator focused on transportation, storage, and logistics across North America. The company has been actively reshaping its portfolio, emphasizing crude oil assets while divesting parts of its natural gas liquid business to streamline operations and improve focus. Its most recent results, reported for the fourth quarter and full year 2025, show a business that remains operationally solid. Net income reached $342 million for the quarter and $1.4 billion for the full year (an 86% increase from 2024), while operating cash flow totaled $785 million in the quarter and $2.9 billion for the year. Adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) came in at $738 million for the quarter and $2.8 billion for the year. Management also guided to roughly $2.8 billion in adjusted EBITDA for 2026 and expects about $1.8 billion in adjusted free cash flow, alongside a 10% increase in its annual distribution. That brings us to valuation.

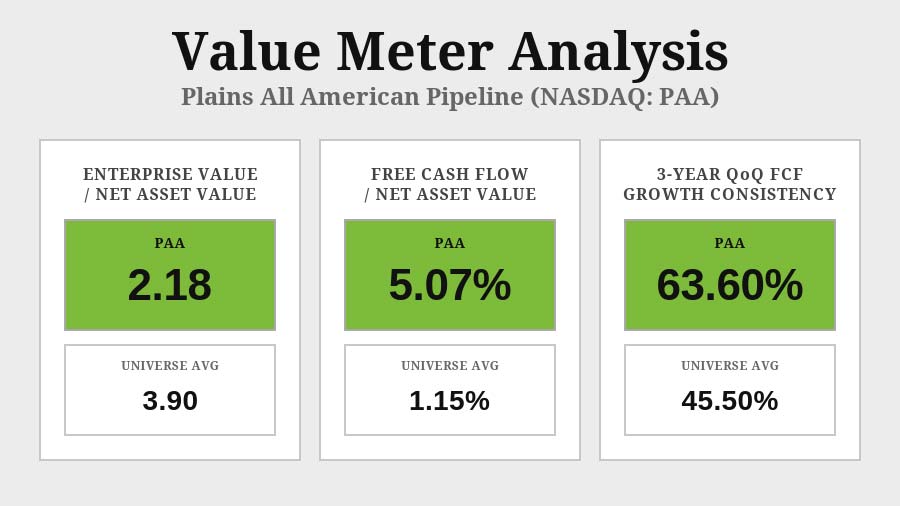

Plains currently trades at an EV/NAV ratio of 2.18 – well below the broad market average of 3.9. In other words, investors are paying significantly less for each dollar of assets compared with the typical company. This discount suggests the market remains cautious about the durability of midstream companies’ earnings despite their stable asset bases.

Plains All American: A Solid Energy Value Play appeared first on

Wealthy Retirement.

Source:

https://wealthyretirement.com/income-op ... source=app